What Is Holding Back Foreign Investment in Mongolia’s Mining Sector—and Can Royalty Rates Reform Fix It?

Feb 23, 2026

Enkhjin A., Zolbayar E.

Mongolia sits atop some of the world's most significant untapped copper and coal deposits. Yet despite this geological wealth, foreign investment in the mining sector has stalled. The culprit? A fiscal regime that investors increasingly view as unpredictable and uncompetitive.

Public consultations on draft amendments to the Mineral Resources Law were underway nationwide, with revised legislation slated for submission to the State Great Khural during the spring session. The proposed reforms target four persistent barriers that have dampened investor appetite: excessive royalty rates, double taxation, levies on associated minerals, and inadequate benefit-sharing with mining-affected communities.

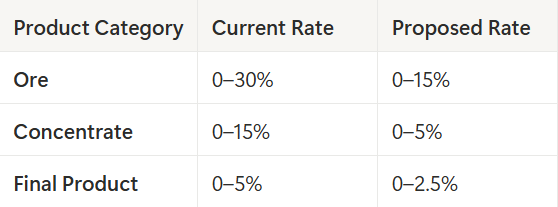

1. Royalty Rates: Closing the Competitiveness Gap

Mongolia’s current royalty structure places it among the world’s most expensive mining jurisdictions. Copper faces a base royalty of 5%, but progressive surcharges tied to product type can push effective rates to 22–30%—more than triple comparable regimes in Australia’s Queensland, Western Australia, New South Wales, where copper royalties range from 2.5% to 7.5% depending on the type and average metal prices.

The proposed amendments would substantially reduce this burden:

This tiered reduction serves a dual purpose: lowering the overall fiscal take while preserving incentives for domestic value-addition. Companies producing refined products in-country would face the lowest rates, aligning fiscal policy with Mongolia’s industrialization objectives.

2. Eliminating Double Taxation on Exports

Under the current regime, exporters may face overlapping royalty obligations on the same mineral output—both as raw ore and as a processed concentrate or final product. This structural flaw increases fiscal pressure and complicates project economics.

The draft amendment addresses this through revised language in Article 47.7: mineral resource royalties “shall not be subject to double taxation” when minerals are exported directly as a product or as value-added concentrates and products.

3. Exempting Associated Minerals

Many ore bodies contain secondary elements recovered incidentally during extraction of the primary commodity. Under current law, these associated minerals can trigger additional royalty obligations, even when they represent marginal economic value.

The proposed Article 47.20 would exempt such elements from royalty calculations, provided they are associated elements of the primary mineral.

4. Strengthening Local Benefit Distribution

The amendments propose channeling 20% of total royalty revenues directly to the soum (local district) where the project is located, with an additional 10% allocated to the host aimag (province). This structural commitment to infrastructure, public services, and long-term community development could meaningfully shift local attitudes toward optimistic views and new projects.

Separately, Mongolia has finalized a new framework requiring 60% of economic returns from strategic mineral deposits to flow into its National Sovereign Wealth Fund—ensuring the majority of resource benefits accrue directly to the public.

Investment Outlook: Reform Is Necessary, but Not Sufficient

Several significant projects await capital deployment. The Nariinsukhait coal deposit and the Kharmagtai copper project are either exploration-ready or approaching development decisions. Yet persistent policy uncertainty continues to weigh on foreign investor confidence. The unresolved question of state equity participation—ranging from 34% to 51% under various proposals—remains a particular concern.

According to Think Mongol Institute, beyond these advanced-stage assets, a more fundamental problem is emerging: exploration activity has stagnated. Without sustained investment in early-stage exploration, the pipeline of future deposits is not being replenished. Mongolia's current project inventory reflects discoveries made years or decades ago; the next generation of mines cannot be developed if they are never found. Attracting foreign capital is therefore a prerequisite for sustaining Mongolia's mining sector beyond its current project inventory.

Royalty rates reform addresses real structural problems. Lower royalty rates, elimination of double taxation, and clearer treatment of associated minerals would collectively improve project economics and reduce fiscal complexity. Enhanced local revenue-sharing could help secure community support for new developments.

But reform alone cannot restore confidence. What investors ultimately seek is regime stability—a credible commitment that the rules governing multi-decade capital deployments will not shift with each political cycle.

Mongolia possesses globally significant mineral reserves. The question is whether its policy environment can become equally competitive. The spring session’s legislative outcome will signal whether Mongolia is prepared to translate geological potential into sustained foreign investment—or whether promising deposits will remain stranded by political risk.

Loading ...

.png)