The Century Belongs to Whoever Owns the Compute

Mar 23, 2026

Soronzonbold Otgonbaatar, Sangaamaa Enkhtuvshin, Lkhamsuren Altangerel, Battsengel Baatar

Sovereign compute infrastructure is emerging as the defining strategic asset of the AI era. Geography, energy, cooling physics, and export controls will determine who captures value and who remains dependent.

Every era has its defining infrastructure. Roads built empires. Railways made economies. Power grids gave us the modern world. What we built them with kept changing: stone, steel, fiber optics. But the point of infrastructure never did. It makes people productive. That is what infrastructure has always done.

So what is the infrastructure that matters now? Compute.

We are already in the exascale era. Supercomputers are performing 10¹⁸ floating-point operations per second. Countries compete over who has the most powerful system, the greenest one, and the most strategically significant one. These are not vanity projects. This is how knowledge gets created in 2026: drug discovery, climate modeling, materials science, and AI. A theory is tested in simulation, stress-tested at scale, refined, and deployed. What once took years in a lab can now take hours on a large cluster. The knowledge economy does not run only on ideas. It runs on the machines that test them.

And while much of the world was not paying attention, the race went private. OpenAI, Anthropic, Google, xAI, and others are building supercomputing infrastructure that increasingly rivals the strategic importance of state systems. NVIDIA chips are now subject to export controls. Governments are debating access to advanced accelerators as a geopolitical issue. Compute stopped being a technical detail somewhere around 2023. It is now a sovereignty question.

So the question that matters is simple: who owns your compute?

The colony problem, digital edition

Most developing countries today are digital tenants. Every model they train, every inference they run, every dataset they process ultimately depends on someone else’s machines, in someone else’s jurisdiction, at prices someone else sets.

Many national AI strategies still focus on talent development, pilot programs, and innovation workshops. All of that matters. But none of it resolves the structural issue if the underlying compute base remains external.

You cannot build sovereignty on rented GPUs. No country would build its energy strategy on importing 100% of its electricity from a neighbor. Yet that is effectively what many countries are doing with compute.

Dependence on external compute means dependence on external pricing, external policies, external capacity ceilings, and external political conditions. In a supply-constrained AI market, that is not a temporary inconvenience. It is a strategic vulnerability.

There is a math problem hiding in plain sight

The AI industry keeps building in the same places: the established hubs of the Global North. These locations benefit from incumbency, but they also face obvious constraints: rising land prices, growing power stress, and expensive cooling infrastructure for increasingly dense GPU clusters.

Now consider the Gobi Desert. Solar irradiance comparable to major desert regions. Some of the strongest wind resources in the world. Winters that reach –30°C, enabling natural cooling conditions that hot-climate data centers must simulate at far higher cost. Vast land availability. Geographic proximity to major Asian markets.

And Mongolia is not unique in this regard. Central Asia, parts of the Sahel, and Patagonia all demonstrate the same point: the physics works in more places than the industry currently acknowledges. Cheap renewables, cold air, open land, and the ability to build without fighting dense legacy infrastructure are not marginal advantages. They are strategic ones.

Problem matters. Scale matters.

The countries that own their compute will create knowledge on their own terms. They will test their own theories, build AI systems aligned to their own industrial structure, and solve their own problems in energy, mining, agriculture, logistics, and finance.

Countries without their own compute base will rent their intelligence. They will remain subject to someone else’s pricing, someone else’s limits, and someone else’s willingness to serve them when demand spikes or geopolitics shift.

Mongolia does not have to accept that. And, more broadly, neither does most of the developing world. But that requires building real infrastructure in real places rather than stopping at policy rhetoric and presentation slides.

The argument, then, is not merely that compute is important. It is that control over compute is becoming a foundational layer of economic agency.

Selected exhibits

The following exhibits provide the empirical context for the argument above, based on publicly available sources current to March 2026.

Exhibit 1

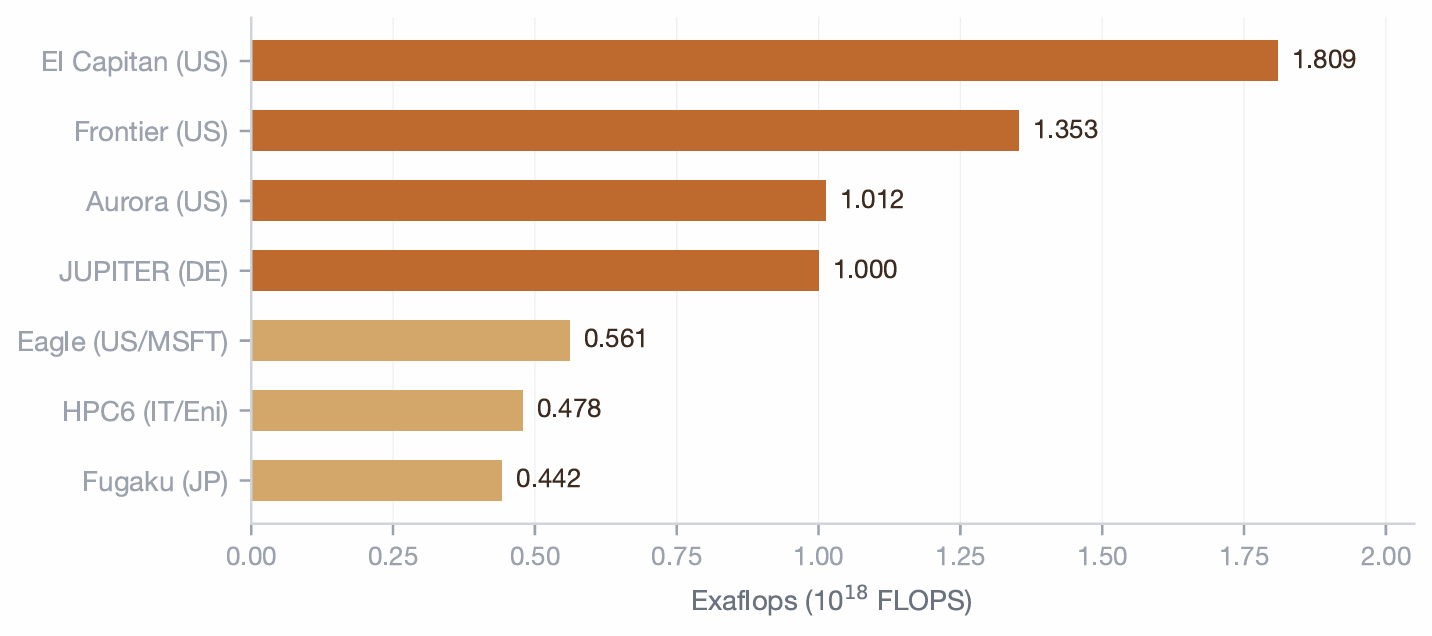

Three of the world’s four exascale systems are in the United States

TOP500 verified supercomputer performance, Exaflops (10¹⁸ FLOPS), November 2025

Note: China is believed to operate 2–3 exascale systems but stopped submitting to TOP500 in 2023. Germany’s JUPITER ranks #1 on the Green500 for energy efficiency.

Source: TOP500.org, November 2025; HPE Newsroom

Exhibit 2

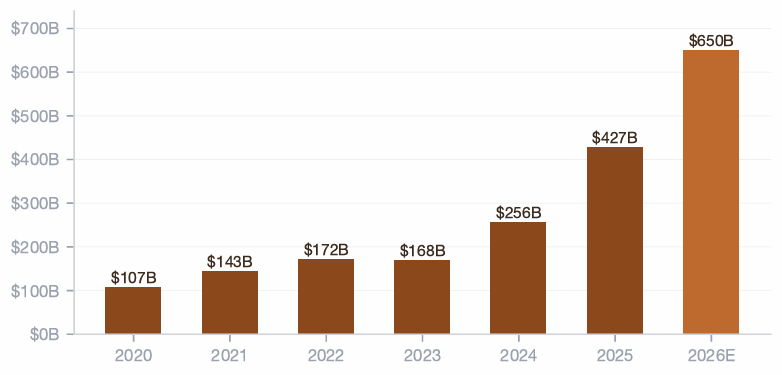

Big Tech’s AI infrastructure spending has increased sixfold in six years — and is still accelerating

Combined capital expenditure of Amazon, Alphabet, Meta, Microsoft, and Oracle, $ billions

Note: Approximately 75% of 2026 spending targets AI infrastructure — GPUs, servers, and data centers. Capital intensity has reached 45–57% of revenue, resembling utility companies rather than traditional tech firms.

Source: RBC Wealth Management; Bridgewater Associates via Reuters; Goldman Sachs Research; company earnings reports

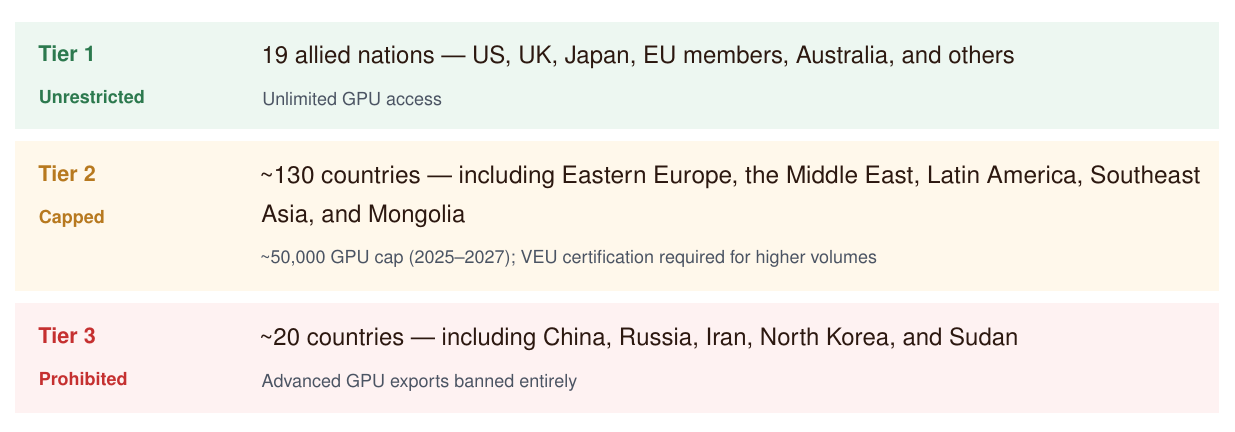

Exhibit 3

US GPU export controls have created a three-tier world for access to advanced AI hardware

Note: As of March 2026, the Trump administration is drafting rules that would require US Commerce Department approval for AI chip exports to any country worldwide, including close allies. NVIDIA’s data center revenue reached $115B in FY2025 — the overwhelming majority from outside the US.

Source: Bureau of Industry & Security; Congressional Research Service (R48642); Greenberg Traurig LLP

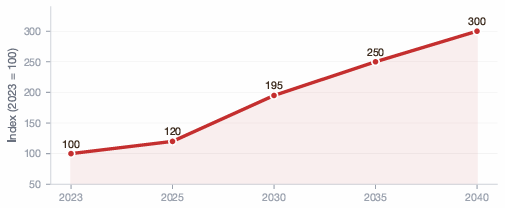

Exhibit 4

Data center power demand is projected to nearly triple Virginia’s electricity consumption by 2040

Indexed electricity demand in Virginia (2023 = 100), driven almost entirely by data center expansion

Source: JLARC Virginia Data Center Report; PJM Interconnection; Dominion Energy IRP 2025; American Action Forum

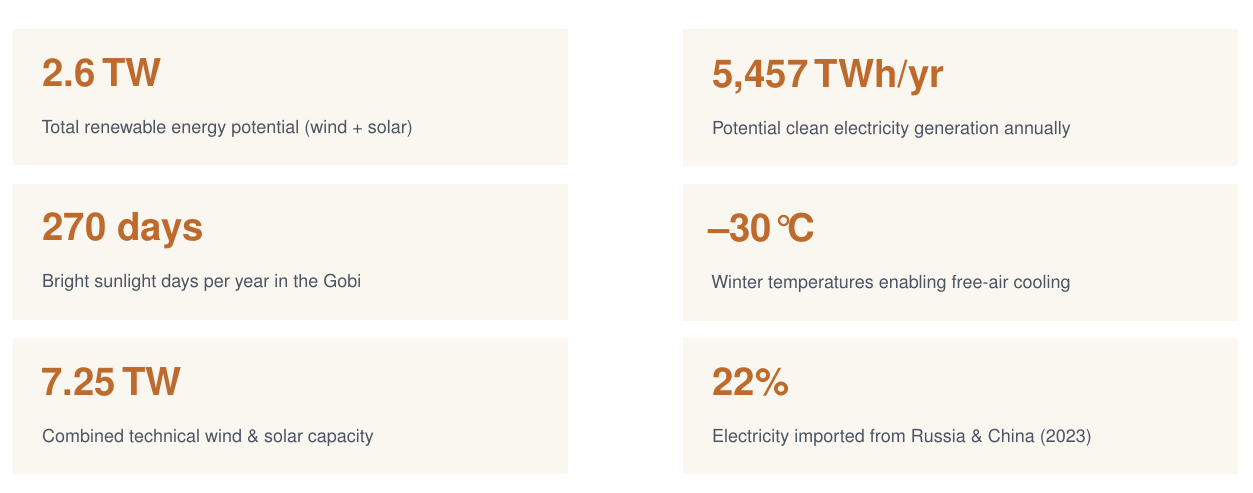

Exhibit 5

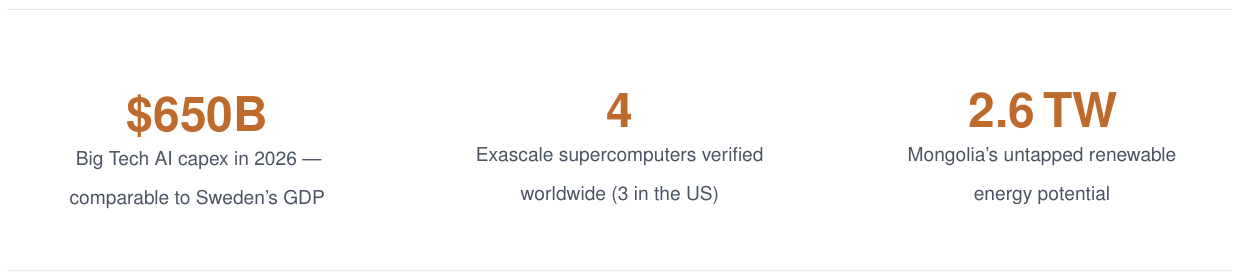

Mongolia’s renewable energy potential exceeds total US electricity consumption

Key metrics for data center siting advantage in the Gobi Desert

Note: Finland’s LUMI supercomputer already demonstrates the model: 100% hydroelectric power, natural Arctic air cooling, waste heat recycled to warm nearby buildings. It ranks among the top 5 globally while running on entirely renewable energy.

Source: IRENA Renewables Readiness Assessment; National Renewable Energy Center of Mongolia; ADB; EU Delegation to Mongolia; ScienceDirect

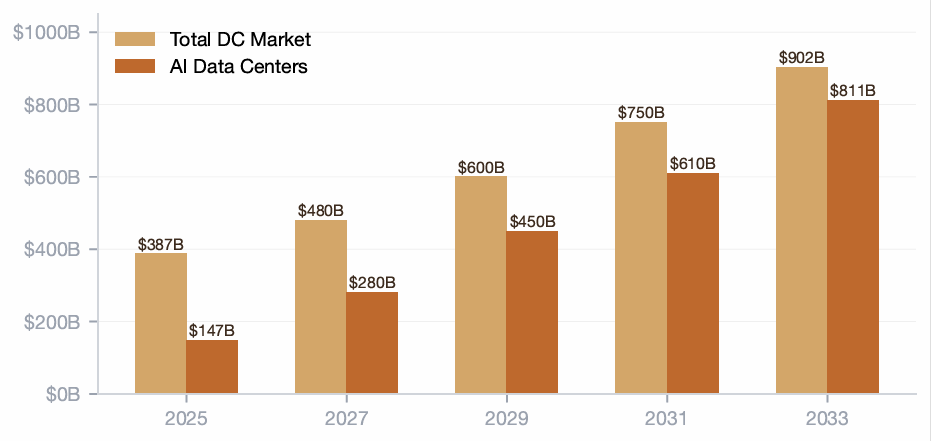

Exhibit 6

The global data center market is on track to become a $1 trillion industry — and AI is driving most of the growth

Global data center market vs. AI-specific data center market, $ billions

Source: Precedence Research; Grand View Research; Fortune Business Insights; Industry Forecast News (March 2026)

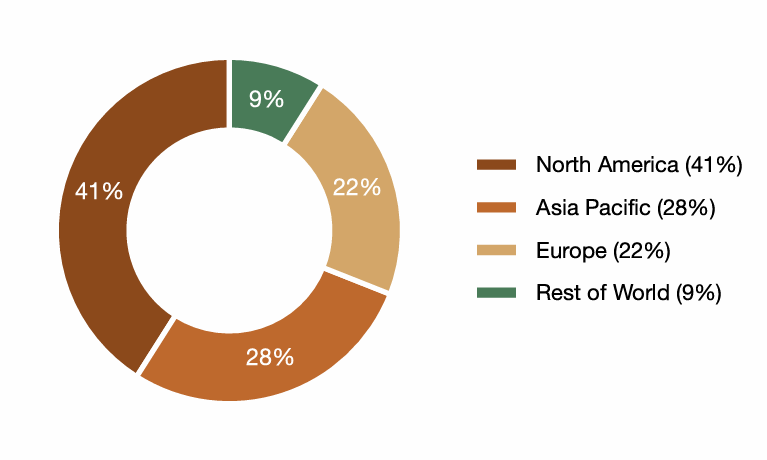

Exhibit 7

Nine percent of the global data center market serves the entire developing world

Regional share of global data center market revenue, 2025

Note: “Rest of World” — including all of Africa, Central Asia, and most of South America — accounts for just 9% of global data center capacity. This is the sovereignty gap. Asia Pacific is the fastest-growing region, but growth is concentrated in established hubs such as Singapore, Tokyo, and Sydney rather than frontier markets.

Source: Precedence Research; Grand View Research; Statista

ABOUT THE AUTHORS

Soronzonbold Otgonbaatar, Sangaamaa Enkhtuvshin, Lkhamsuren Altangerel, and Battsengel Baatar.

The authors bring together PhD-level expertise in quantum computing and artificial intelligence, international capital markets experience, and strong academic and institutional partnerships.

METHODOLOGY & SOURCES

Supercomputer rankings from TOP500.org (November 2025 list). Capital expenditure data from company earnings reports, RBC Wealth Management, Goldman Sachs Research, Bridgewater Associates analysis via Reuters, and Futurum Group. GPU export control framework from the US Bureau of Industry & Security, Congressional Research Service report R48642, and Greenberg Traurig legal analysis. Virginia power data from JLARC Data Center Report, PJM Interconnection, Dominion Energy 2025 Integrated Resource Plan, and American Action Forum. Mongolia renewable energy data from IRENA Renewables Readiness Assessment, National Renewable Energy Center of Mongolia, ADB Mongolia First Utility-Scale Energy Storage Project RRP, EU Delegation to Mongolia, and ScienceDirect geospatial assessment (2022). Data center market sizing from Precedence Research, Grand View Research, Fortune Business Insights, Statista, and Industry Forecast News (March 2026). All figures represent the most recent available data cited in the article. Projections and estimates should be interpreted as directional forecasts rather than precise outcomes.

Loading ...

.png)