Mongolia's Hidden Emerging Strategic Asset Amid a Global Supply Chain Crisis

Apr 20, 2026

Ariunzaya B.

The global sulphur and sulphuric acid market is entering a period of acute stress. The Strait of Hormuz carries nearly half of global seaborne sulphur trade, and military escalation has disrupted this flow at a critical moment. Prices surged over 600% to $531/tonne by January 2025, reaching $600–800/tonne post-Hormuz. Sulphuric acid sits at the core of industrial value chains critical to fertilizer production, metals processing, oil refining, and chemical manufacturing.

On April 10, China by far the world's largest producer of sulphuric acid, largely as a byproduct of copper and zinc smelting effectively curtailed exports. While not formalized as an official blanket ban, market guidance indicates a de facto suspension of its 2.7 million annual export tonnes from May 1, prioritizing domestic fertilizer production during peak agricultural demand. Russia has adopted similar protective measures on upstream technical sulphur exports through June. The FAO warns fertiliser prices could rise 15–20% in H1 2026. That the world's two largest producers are choosing food security over export revenue signals how serious the shortage has become. Two of the largest suppliers have shifted from export maximization to domestic security tightening global availability and reinforcing upward pressure on industrial input costs, with second-order effects on food inflation and mining economics.

What this means for Mongolia?

In the near term, Mongolia appears relatively insulated and even advantaged. Most of the copper exported as concentrate to the Chinese market, avoiding large volume domestic demand for sulphuric acid in primary production. While Chile's acid-dependent SX-EW copper (20% of its output) and Africa's import-dependent mines face mounting pressure, Mongolia's copper output continues to be largely uninterrupted. The global shortage that is hurting competitors is, paradoxically, boosting Mongolia's revenues.

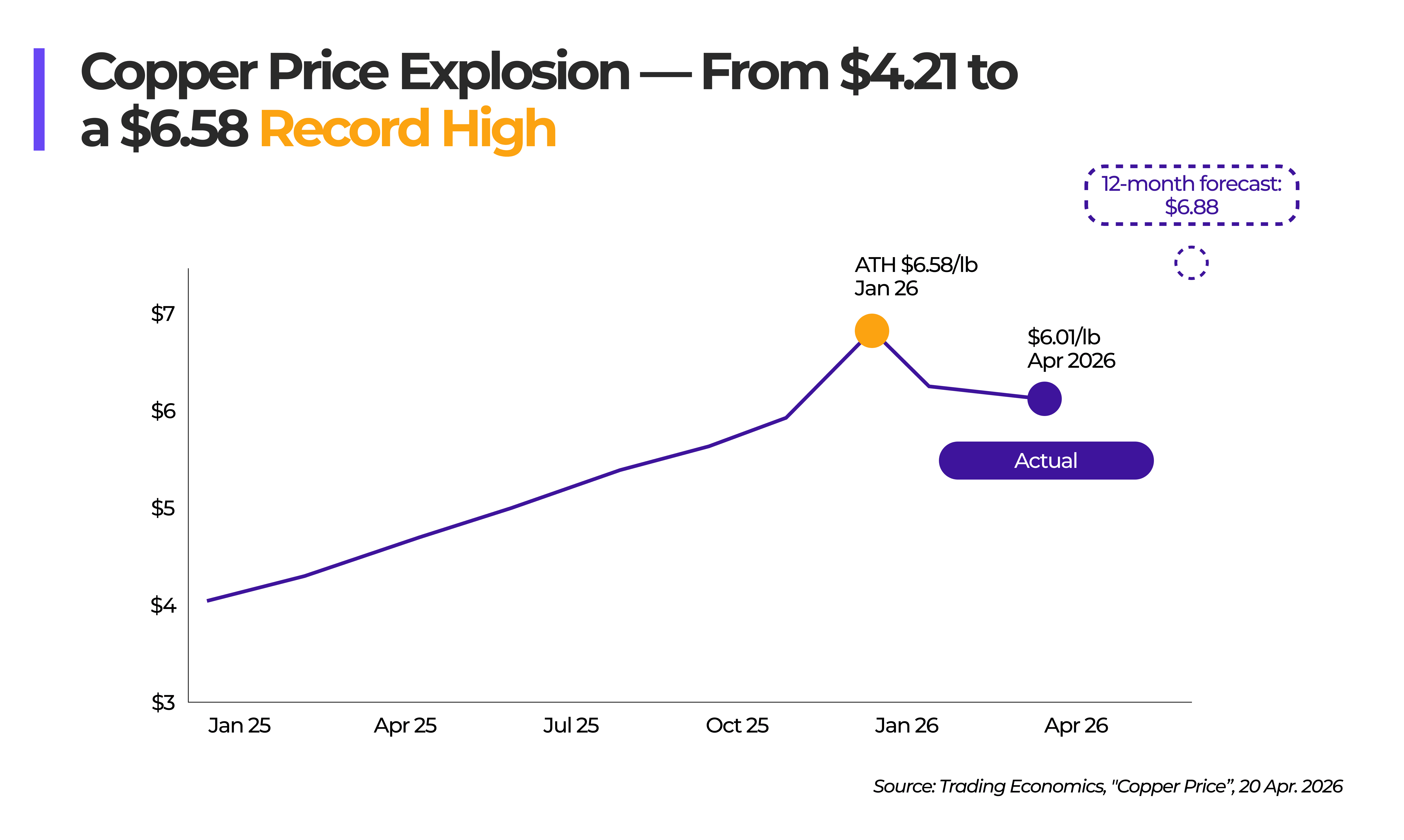

Copper was trading at $6.01 per pound on April 20, 2026 almost 30% higher than a year ago and is forecast to continue rising as supply constraints from the sulphuric acid crisis tighten competitor output. Which means value and volume for copper exports will rise significantly in 2026 as in 2025 copper exports were valued at $5.83 billion saving the state budget.

Mongolia imports nearly all of its sulphuric acid predominantly from Russia to support limited domestic leaching operations such as Achit Ikht and Erdenet. This creates a circular dependency: Mongolia exports the underutilized raw material, yet remains structurally reliant on external suppliers for the finished product. As global supply tightens and prices rise, this model becomes increasingly inefficient and strategically exposed.

Recent trade data confirms early-stage repricing. Import prices for sulphuric acid into Mongolia have already trended upward into 2026, reflecting broader market dynamics. While Russia continues to supply acid, its own production constraints and export prioritization policies introduce medium-term reliability risks. A supply chain anchored to a single external partner, particularly one facing its own upstream pressures represents a clear concentration risk.

The Inflection Point: Two Projects, One Supply Chain

The urgency lies not in current consumption, but in projected demand. The Zuuvch Ovoo uranium mine, a $1.6 billion investment agreement signed with France's Orano Group on January 17, 2025 uses in-situ leach mining, which relies on sulphuric acid as its primary extraction reagent. Mongolia's consumption is set to increase fifteen to twenty times from current levels. The investment agreement includes a planned dedicated acid plant, but securing consistent sulphur feedstock in a tightening global market remains a critical execution risk.

At the same time, the long-delayed Erdenet copper smelter Mongolia's 40-year industrial ambition, now finally in active tender with four shortlisted companies including Glencore and Chinese giants ,presents a structurally aligned solution. The Erdenet copper smelting and refining plant is capable of supplying 40% of the elemental sulfur it produces to a new sulfuric acid plant, sufficient to meet Zuuvch Ovoo's increased demand. Once operational, the smelter would produce 988,000 tonnes of sulphuric acid per year as a byproduct enough to supply Zuuvch Ovoo entirely and potentially create export capacity. One project's byproduct is the other's critical input. Together they form a domestic supply chain that would end Mongolia's dependency on Russia completely.

This alignment fundamentally changes the project economics. In 2016, experts calculated that only 25% of the smelter's acid byproduct could be absorbed domestically making the project infeasible. That constraint has now reversed. Global shortages, rising prices, and the emergence of large-scale domestic consumers have transformed sulphuric acid from a byproduct liability into a strategic asset. The world is now scrambling for sulphuric acid, and for the first time Mongolia has the raw materials, the projects, and the demand to justify production at scale.

Conclusion: Strategic Timing, Not Structural Constraint

The clock is running. Zuuvch Ovoo begins production by the end of 2028 but the smelter's tender remains unresolved as of April 2026, with four international companies shortlisted and a winner yet to be selected. If construction does not begin soon, the 2028 acid demand will arrive without a domestic supply to meet it, forcing Mongolia back to expensive outside purchases. A sustained sulphuric acid supply crisis would transmit directly into mining input costs, uranium project timelines, and agricultural costs , compounding inflation already projected by the ADB to rise to 7.8% in 2026. This creates a feedback loop: commodity-driven growth remains strong, but the inputs required to sustain that growth become increasingly constrained and expensive.

Mongolia is not structurally disadvantaged, it holds the raw materials, project pipeline, and industrial logic required to build a fully integrated sulphur-to-acid value chain. The current global dislocation is not just a risk; it is a signal. As major producers prioritize domestic needs and supply chains fragment, countries with latent integration opportunities have a narrow window to reposition. The sulphuric acid war has not yet started but for the first time, Mongolia has a real chance to win it independently of both neighbours. The raw materials exist. The demand is confirmed. The policy framework is in place. What remains is the decision to connect them before 2028 makes it urgent and before the market makes it expensive.

Loading ...

.png)