Mongolia's Tungsten: The Processing Gap Investors Should Know

Jun 9, 2026

Ariunzaya B.

China controls over 80% of the world's tungsten supply. On February 4, 2025, Beijing made that number matter. Export controls on tungsten, covering not just raw ore but ammonium paratungstate (APT), the refined intermediate that manufacturers actually buy, sent buyers across the United States, Europe, South Korea, and Japan scrambling. Non-Chinese tungsten did not merely become valuable. It became strategic.

Why Tungsten, Why Now

Tungsten sits at the intersection of every industry that currently defines geopolitical competition. Militaries depend on it for armor-piercing munitions and missile components, and there is no substitute. On the commercial side, every electric vehicle contains roughly 2,000 semiconductors, and tungsten wiring runs through all of them. Defense budgets are rising. EV production is scaling. Demand is climbing from both directions at once, and the world's dominant supplier has just restricted access.

Markets responded before policy did. APT prices broke records within weeks of Beijing's announcement, repricing non-Chinese tungsten as a strategic asset overnight. What followed was more deliberate but no less significant: the United States, South Korea, Germany, and Japan each began directing capital toward alternative supply chains. The political will to fund non-Chinese tungsten is now at a historic high.

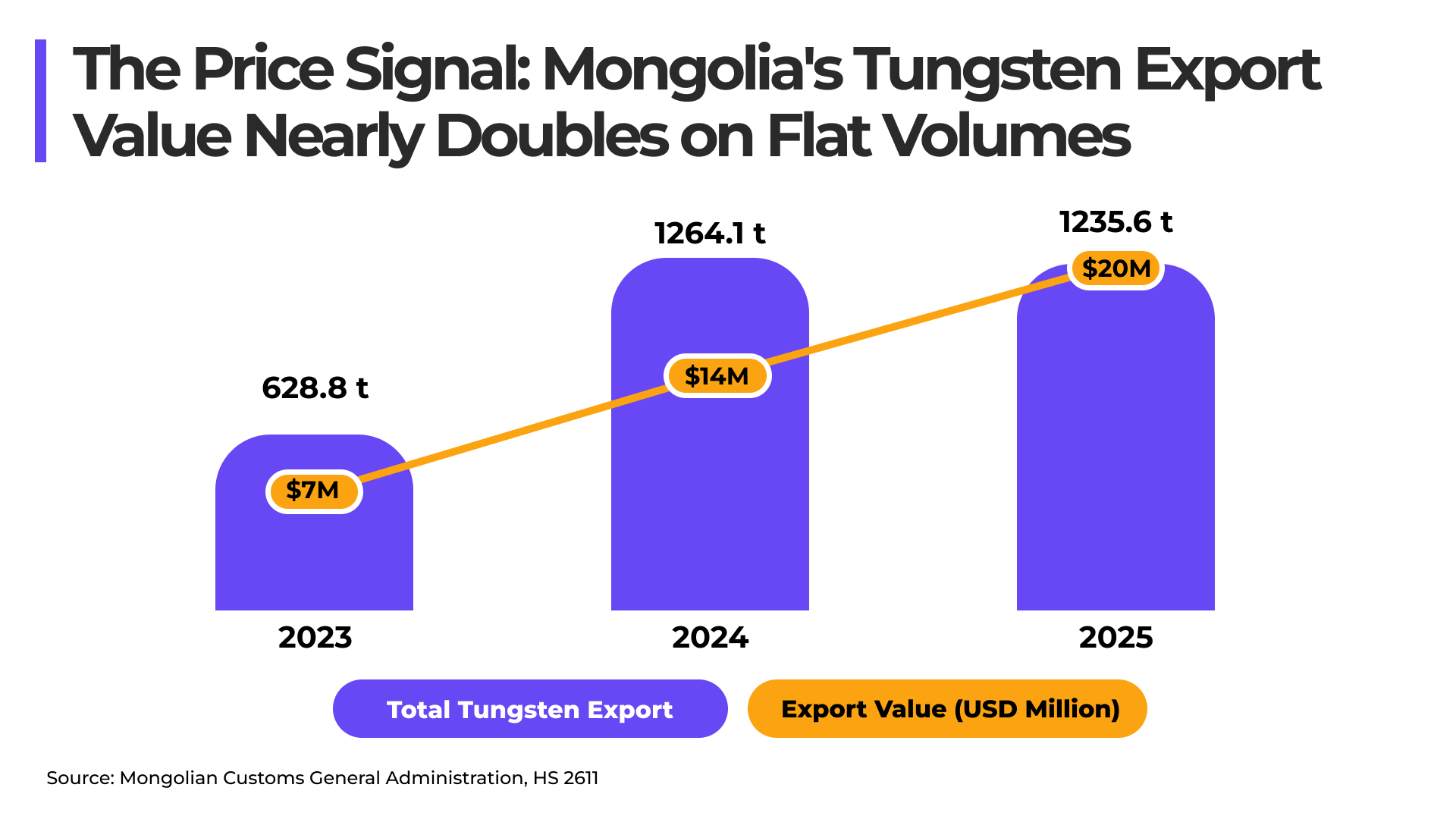

Mongolia Has What the World Needs

Mongolia is not a marginal player. The USGS recognizes its tungsten reserve at 4,300 metric tons, with producing operations already running at Erdenetiin-Ovoo and the Khovd River Mine. A June 2025 peer-reviewed study in Minerals, using KIGAM data, confirmed Mongolian ores fall within the upper range of the global grade band and identified a viable renewable energy pathway for domestic processing.

The buyer shift is already visible. Export value climbed from $14 million to $20 million between 2024 and 2025 on flat volumes. China's share fell from roughly 90% to 75% in a single year. The United States entered as a meaningful buyer for the first time. South Korea received its first shipment. Germany purchased consistently. Japan entered in 2026. The diversification is real, and still early.

The Gap That Matters

Mongolia has geology. It does not yet have the refining infrastructure, and that is where the value chain pays. APT, the processed intermediate that fabs, defense contractors, and EV manufacturers actually purchase, commands substantially higher margins than raw ore. Mongolia currently lacks domestic APT capacity, meaning its ore flows largely into China's refining system: the same system that just imposed export restrictions on the product it produces.

The dependency is historical. For years, nearly all exports went to China, leaving no incentive to build domestic processing. When demand collapsed in 2020, China pulled back and Mongolia had nowhere else to go. The lesson from that episode was not acted on. This one needs to be.

The Window Is Open

Policy is moving. Mongolia's Cabinet approved Minerals Law amendments in May 2026 introducing a dedicated beneficiation license and a statutory critical minerals list covering 21 types. The bill is before Parliament now. Diplomatically, the US-Mongolia-South Korea trilateral framework has been operational since June 2023, with a Korea-Mongolia rare metals cooperation committee launched in November 2023. The KIGAM research gives investors the independent technical validation they need before committing capital.

APT processing is an industrial build-out, not a short-term trade. It takes years to reach commercial scale, which means the time to move is now, before the capacity exists and before it gets bid up by a crisis that has already arrived. The geology is there. The buyers are there. The policy framework is forming.

Mongolia does not need to dominate global tungsten production to matter. It only needs to become credible. The rest of the world is already looking.

Loading ...

.png)