Blue Finance 101: Why Invest in Water, How to Design Blue Finance Products, and Start Investing in Water

Jun 25, 2026

Nandin-Erdene E.

Photo credits: Copyright © Daesung Lee. All rights reserved

Water is the only resource on Earth with no substitute. You cannot engineer a replacement, grow food without it, or keep a city running on an alternative. When oil becomes scarce, economies adapt. When water becomes scarce, civilizations collapse. That irreplaceability is the entire investment thesis.

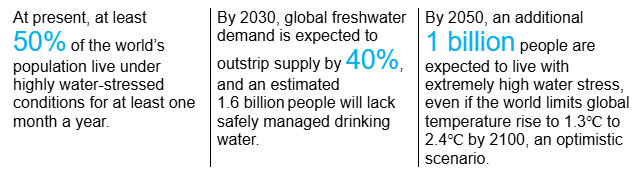

The scale of the water crisis is staggering, yet so is the economic logic for solving it. Nine out of 10 climate events are water related (World Bank, 2023). Droughts and floods continue to grow in intensity, groundwater is drying up, cities and farms are facing water shortages, and glaciers are melting at an accelerated pace. Some 80% of wastewater from industry and municipalities is discharged without treatment, quietly poisoning the water systems the global economy depends on (World Bank, 2020). The Global Commission on Adaptation warns that failing to implement better water management could wipe out 7 to 12% of GDP across Central Asia, China, and India alone (WEF, 2023).

And yet the World Resources Institute has found that fixing the problem globally costs roughly 1% of GDP, or just 29 cents per person per day (WRI, 2020). This is perhaps the most compelling risk-reward calculation in infrastructure investment: the price of solving the water crisis is a fraction of the price of ignoring it.

In 2021, WWF estimated the global economic use value of water at US$58 trillion, equivalent to the combined GDP of China, USA, India, Germany, and Japan. The Morgan Stanley finds that water solutions rank #1 globally for investor interest in both the US and Europe.

Mongolia: Vanishing water sources and the financing landscape

Mongolia is already living the water crisis that much of the world fears. According to the WRI's Aqueduct Water Risk Atlas, the country faces "high water stress," withdrawing 40–80% of its available supply. The glaciers that feed that supply are disappearing fast, losing more than a third of their area since 1990, with lower-elevation glaciers below 3,600m losing 70% in the same period. Permafrost, which acts as a natural water store across much of the landscape, has shrunk by 34% since the 1970s (Fengjiao et al., 2025) The human cost is already visible in the capital: 40% of Ulaanbaatar residents have no running water at home, and 80% lack access to municipal sanitation.

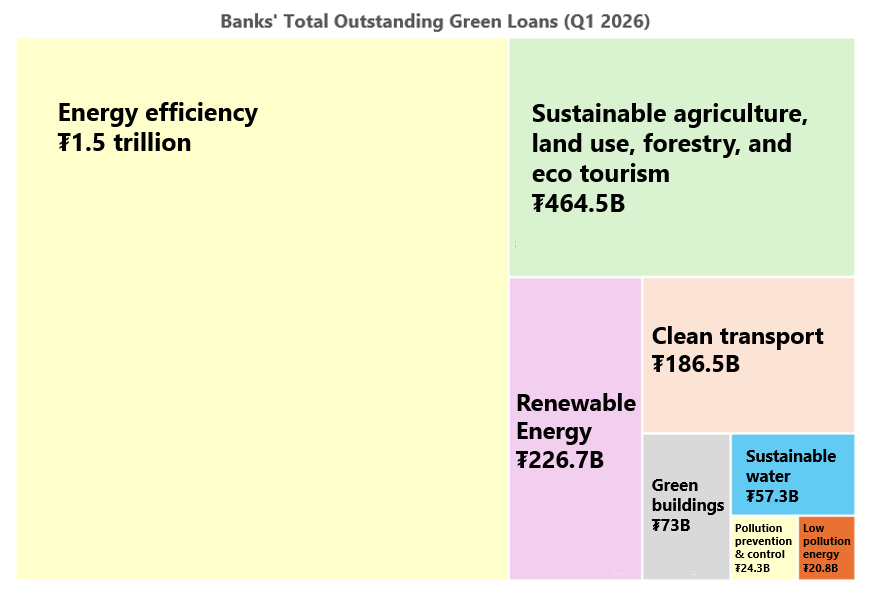

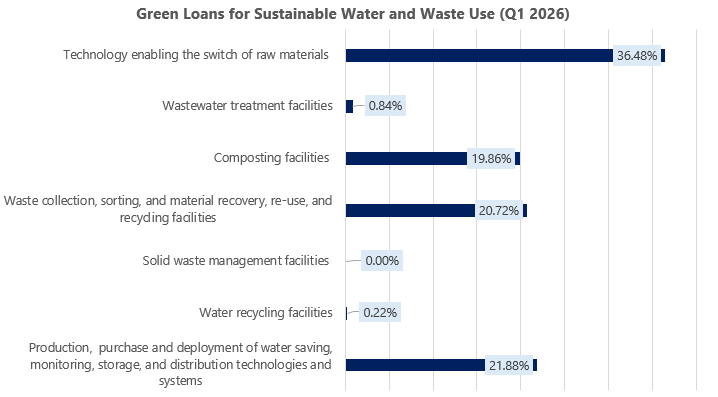

Mongolia's National Sustainable Finance Roadmap sets clear targets: Commercial banks must grow their green loan portfolios to at least 10% of total lending, and non-bank financial institutions to 5%, both by 2030. Progress is underway — as of Q1 2026, banks hold MNT 2,550 billion (approximately US$713 million) in outstanding green loans, representing 5.7% of total lending. But water remains marginal within that portfolio. Just 2.2% of green loans are labelled as sustainable water and waste use, leaving significant room to scale capital toward the country's most pressing environmental challenge.

Source 1. Green Loan Statistics, Central Bank of Mongolia, Q1 2026

Designing Blue Finance Products and Starting to Invest in Water

Turning water-related opportunities into investable assets requires more than a label. Institutions need a clear process for defining eligibility, managing ESG risks, measuring impact, and demonstrating credibility to investors. The following five steps outline a practical approach.

Step 1. Defining blue finance

Blue finance sits within the broader universe of green and sustainable finance, focused specifically on protecting water systems, marine environments, and the wider water economy. Blue finance instruments — whether bonds, loans, or sustainability-linked structures — can fund a wide range of activities: sustainable water and wastewater management, marine biotechnology, shipping and transport, fisheries and aquaculture, habitat restoration, and coastal tourism.

To qualify as a blue financial instrument, two conditions must be met. First, the instrument must comply with the established principles governing its structure — the Green Bond Principles, Green Loan Principles, Sustainability-Linked Bond Principles, or Sustainability-Linked Loan Principles, depending on the instrument type. Second, it must align with the Blue Guidance Framework set out in IFC's Guidance for Blue Finance 2.0. Together, these requirements ensure that blue-labelled instruments meet recognized standards and direct capital toward genuine environmental outcomes.

Step 2. Identifying eligible blue finance activities

For an activity to qualify as blue finance, activities should make a meaningful contribution to sustainable water management or the protection of freshwater and ocean ecosystems. It should also deliver outcomes that can be measured and reported; and it should align with IFC's Blue Guidance Framework. Mongolian financial institutions can additionally refer to the Mongolia SDG Finance Taxonomy as a national-level reference point.

Step 3. Ensuring ESG safeguards

An activity can only carry the blue label if it does not create material risks for other environmental priorities. Compliance with recognized standards — such as the IFC Performance Standards and the World Bank's Environmental, Health, and Safety Guidelines, or equivalent frameworks — is expected as a baseline. Where relevant, industry-specific sustainability standards and product-level standards may also apply, particularly where these set a higher bar than national requirements.

Step 4. Determining blue impact indicators or KPIs

Impact indicators provide a means of evidencing the environmental and social benefits — and co-benefits — generated by blue-eligible activities. While the specific indicators used will vary depending on the nature and scale of the activity and the instrument involved, issuers and borrowers should make reasonable efforts to gather and report impact data, both in allocation reports and in ongoing impact disclosures. Internationally recognized frameworks for this purpose include ICMA's Impact Disclosure Guidance, the IRIS+ Catalog of Metrics, and GRI's Sector Standards. Mongolian institutions can complement these with the Mongolia SDG Finance Taxonomy and the ESG & Sustainability Reporting Guidance for Mongolian Companies as locally relevant references.

Step 5. MRV or External Review

Robust monitoring, reporting, and verification (MRV) is essential to maintaining credibility with investors and demonstrating real-world impact.

- First, define a clear methodology — establish how impact data will be collected, validated, and reported, including the frequency of reporting cycles.

- Second, assign ownership. Designate a specific individual or department responsible for impact monitoring and oversight, and document their role clearly within the organization's governance structure.

- Third, disclose performance. Impact results should be published either as a standalone impact report or integrated into the annual or sustainability report, aligned with both international and national standards.

- Finally, seek external validation. It is strongly recommended to obtain an external review or second-party opinion confirming that the proposed blue instruments are aligned with recognized standards and that proceeds are being used or disbursed correctly. This step materially strengthens investor confidence and the instrument's market credibility.

Loading ...

.png)