What’s Next for Mongolia’s SIBs?

Oct 15, 2025

Tselmeg E.

Mongolia’s capital market has been on quite a transformation journey over the past few years with Banking Reform, OTC Market launch and privatization discussion of state owned companies. The Banking Reform brought tens of thousands of new investors into the market, turning the Mongolian Stock Exchange (MSE) into part of the national conversation. And the results speak for themselves — total market capitalization doubled from ₮5.98 trillion in December 2021 to ₮12.13 trillion by June 2025, one of the fastest growth periods in our financial history.

💡 Did You Know?

The five systemically important banks (SIBs) now account for 44% of total market capitalization, drive over half of the TOP-20 Index, and are responsible for 57% of all dividends paid to investors in 2024. Bank stocks are no longer individual companies — they are the foundation of Mongolia’s equity market.

Mongolia’s banking boom is rewriting the rules of the market:

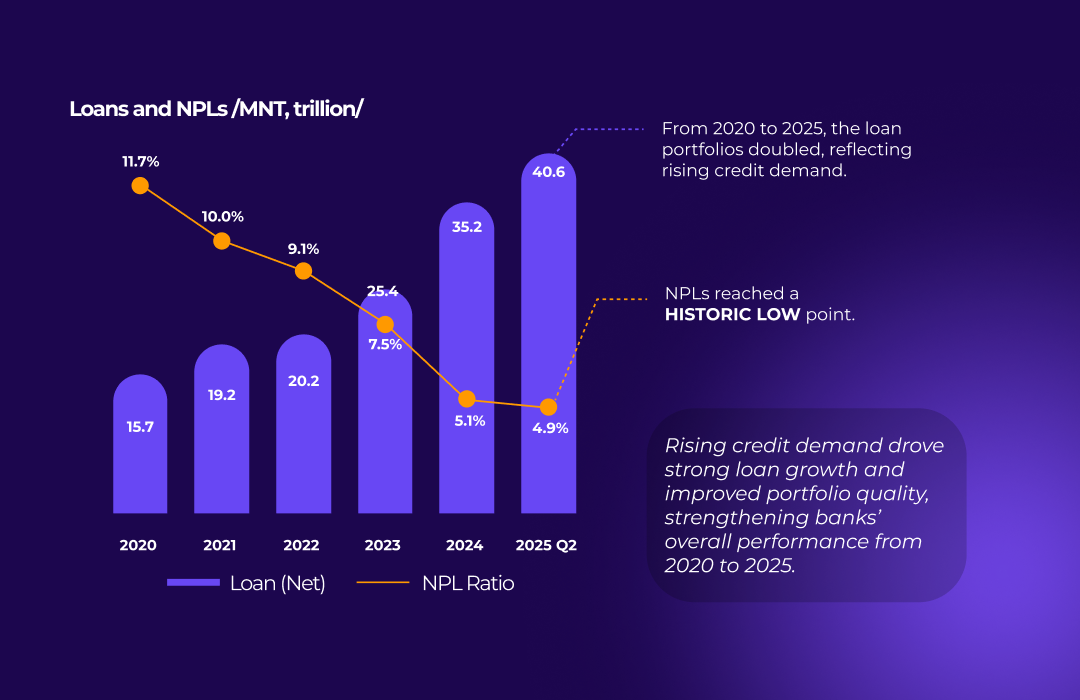

Mongolia’s banks are on a roll — total assets surged to ₮72.6 trillion by Q2 2025, now topping 87% of GDP, while NPLs fell to a historic 4.9%, highlighting both resilience and smarter risk management.

SIBs are not just growing; they’re making serious profits. Khan Bank leads the pack with $5.95 billion in assets and an impressive 29% ROE, while peers are holding steady with 16–22% ROEs, supported by healthy margins and strong loan-to-deposit ratios.

Yet despite this strength, Mongolian banks remain undervalued gems offering attractive dividend yields—Khan Bank 15.3%, Golomt Bank 8.4%, XacBank 5.4%. For investors seeking stable earnings, high yields, and exposure to a rapidly growing economy, Mongolia’s banking sector is a story worth watching.

But today, a critical question emerges: Now that the SIBs are listed, what is the next step?

The IPOs did their job: they opened access to public markets and brought in thousands of new shareholders. But most banks only floated a small portion of their shares, and the real work starts here. The next chapter is about attracting long-term institutional investors, preparing for possible international listings, and raising governance standards to global levels — the kind that truly define world-class public companies.

But here’s where it gets really interesting for investors — the 20% ownership cap on banks hasn’t been fully enforced yet. That means some major ownership shakeups could be on the way.

Regulatory Turning Point: Ownership Rules Under Review:

Back in 2021, Mongolia’s amended Banking Law set a rule: no single shareholder (or related party) can own more than 20% of a bank’s equity. But the deadline for full enforcement was pushed to December 31, 2026, recognizing how complex it is to restructure ownership across the sector.

If this law comes into full effect, all SIBs would be required to reduce any shareholder stakes exceeding 20%, potentially triggering a significant reshuffling of ownership structures. Large shareholders may need to divest or restructure their holdings, while banks could explore strategic partnerships or secondary listings to maintain stability and attract long-term investors.

Proposed Amendments by the Bank of Mongolia (BoM):

The Bank of Mongolia (BoM) has been studying how to make this transition work smoothly and has proposed several key amendments to the Banking Law:

- Raise the Ownership Cap: Increase the existing 20% limit to 51% for publicly listed or predominantly state-owned banks, allowing more flexibility for strategic investors.

- Exemption for International Financial Institutions, subject to parliamentary approval.

- Redefine Significant Shareholders from 5% → 10%.

- Strengthen Governance Rules for executives to avoid conflicts of interest.

These proposals aim to combine greater ownership dispersion, strategic investment flexibility, and stronger governance, representing a major milestone in the evolution of Mongolia’s banking sector.

Are Mongolia’s Banks Ready to Go Global?

Mongolia’s SIBs are now considering strategic investments, international dual-listings on exchanges like HKEX, LSE, or SGX, which can bring:

- Access to global capital and long-term investors

- Higher liquidity and improved valuations

- Enhanced governance and transparency

- Global visibility and market credibility

Mongolia’s banks are performing well at home. But global investors will look beyond the numbers. Governance, ownership transparency, and a clear strategy will be key: aligning reporting standards, strengthening governance, and building investor relations will determine success.

What’s Next for Key Stakeholders Must Do:

- Banks: Strengthen governance frameworks, ensure compliance with international accounting standards, and communicate a clear growth strategy to potential global investors.

- Regulators: Provide clear guidance on ownership rules, streamline compliance mechanisms, and maintain a stable, predictable regulatory environment.

- Investors: Evaluate not just current financials but also long-term governance, transparency, and readiness for cross-border scrutiny.

- Advisors & Partners: Support banks with roadmaps for dual-listing, investor relations programs, and strategic partnerships to attract global capital.

🏁 The Road Ahead:

For Mongolia’s SIBs the global stage will be the ultimate test. Success depends on transparent governance, clear ownership structures, and a compelling long-term strategy and story.

For those ready to act, this is a rare chance to participate in one of the fastest-growing banking markets in the region. Mongolia’s SIBs are no longer just local champions — they are poised to become globally recognized institutions, offering investors a unique gateway to a growing economy.

Loading ...

.png)