Is Mongolia's NBFI Boom Built to Last?

The fastest-growing force in Mongolian finance

For decades, Mongolia's commercial banks held the capital, set the terms, and decided who qualified. High collateral requirements, large minimum ticket sizes, and limited risk appetite left consumers and small businesses outside the system. That exclusion created a gap, and non-bank financial institutions were built to fill it.

According to CMM's newly released Investor's Guide to Mongolia: NBFIs, the sector has grown from 188 institutions in 2011 to 575 licensed operators reaching 78% of all borrowers in Mongolia by number. Three forces explain that reach. NBFIs lend where banks won't, with lower collateral demands and smaller ticket sizes. They lend faster, disbursing to a mobile phone in minutes where banks take weeks.

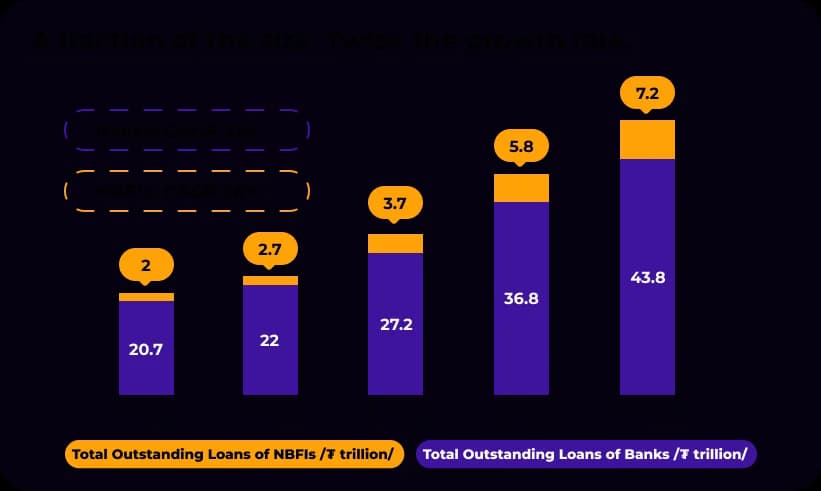

NBFI lending has compounded at 38% annually over the past four years, against 21% for banks, lifting the sector's loan balance to 9.6% of the banking system's and its assets to 14.16% of bank assets. A fraction of the size, twice the growth rate, and steadily rewriting who captures Mongolia's credit growth.

Growth this fast leaves marks

But a sector cannot double its lending pace against banks without consequences. Expanding this fast builds up pressure somewhere in the system, and over the past two years that pressure has surfaced in three places.

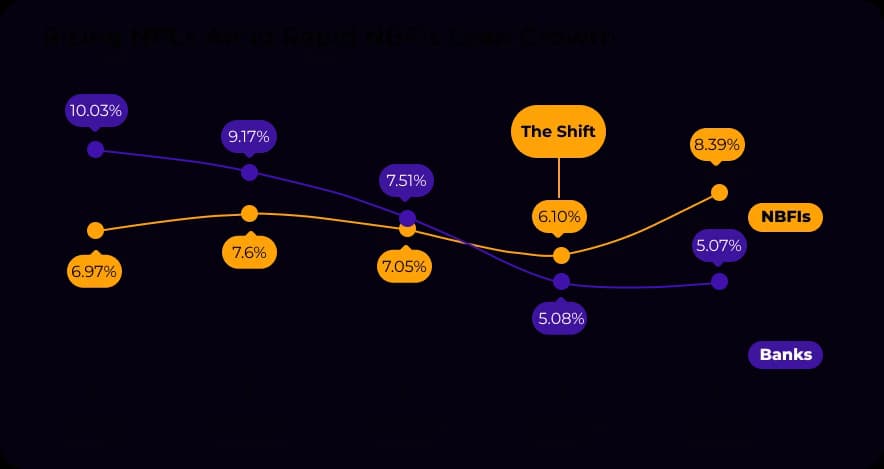

The most visible is asset quality. In 2024, NBFI non-performing loans crossed above bank NPLs for the first time in a decade, reaching 8.39% by end-2025. Lending at speed to borrowers banks excluded carries inherently higher credit risk, and the crossover made that cost measurable.

The second is borrower stress. The sector's expansion has been driven overwhelmingly by loans to individuals, and household debt has risen to levels the IMF flagged in its 2025 Article IV review, alongside concerns about the interconnection between banks and NBFIs.

The third is the regulatory response to those pressures triggered. Between early 2025 and January 2026, the FRC and BoM moved decisively: a ban on NBFIs raising capital from domestic banks, a 60% DTI cap on consumer loans, a 60% loan-to-value cap on auto lending, and a 20% minimum capital adequacy ratio. For a sector of 575 licensed operators, many of them small, the new environment is unforgiving.

The shake-out is also the opportunity

Here is what the headlines miss: just 57 NBFIs, under 10% of licensed institutions, hold 74.1% of sector loans at an NPL ratio below the sector average. The risk sits in the long tail, and the new rules will push those operators out, handing their market share to the institutions built to last.

So the question for investors: who stays?

Three traits separate the survivors.

- Those who invested in the technology. Digital underwriting and mobile disbursement are no longer differentiators, they are the price of entry. The leaders that invested early in sufficient credit scoring models and AI-driven lending can grow while holding credit quality.

- Those who expanded beyond the local market. Operators confined to Mongolia's consumer segment compete in an increasingly crowded and regulated space. Those that took their model abroad, as InvesCore has done with operations in Kyrgyzstan and Kazakhstan, diversified both their revenue and their risk before the tightening arrived.

- Those who can attract foreign capital. With domestic bank funding now off the table, international capital is no longer a growth strategy, it is a survival requirement. The top players moved early: in 2025 alone, InvesCore secured $58 million from investors including FMO, Triple Jump, and Helicap, while LendMN raised over $30 million in debt financing alongside a $21.4 million Series B from IFC. The rest of the sector must now compete for capital the NBFI leaders have already locked in.

Mongolian NBFIs have established a solid foundation for engaging in international deals and securing global funding, and the consolidation now underway will concentrate that strength further. For investors, the entry points span listed shares and bonds, private debt, and strategic equity in a sector where the winners are becoming easier to identify.

🔗 Read the full report, "Investor's Guide to Mongolia: NBFIs," here: https://capitalmarkets.mn/insights/investor-s-guide-to-mongolia-nbfis

To learn more about these investment opportunities, reach out to CMM for expert guidance throughout the investment process.